a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Monthly Publication

Market Review - March 2018

General

Pepper market experienced a declining trend since 2016. In 2017 however, percentage of the decrease was even more sharply by 40% when compare with the decrease of 10% in 2016. This was due to a substantial increase of production and export of pepper in 2017, mainly from Viet Nam and Brazil. Total production and export of pepper in 2017 increased by around 20%, a significant increase when compares with the increase of around 5% in 2016.

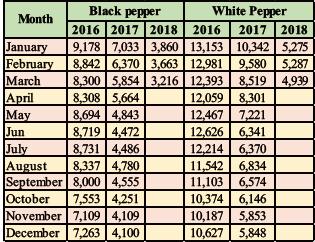

In 2017 composite price decreased by 42% for black from US$ 7,033 per Mt in January 2017 to US$ 4,100 in December 2017; while that for white pepper the price decreased by 43% to US$ 5,848 per Mt in December from US$ 10,342 in January 2017. Average composite price of pepper in 2017 was US$ 5,043 per Mt for black and US$ 7,327 per Mt for white pepper as against US$ 8,253 and US$ 11,811 per Mt for black and white pepper respectively in 2016.

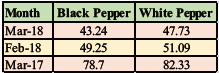

In March 2018, the market continued to show a declining trend. Pepper price index decreased by 6.01 points for black pepper and 3.36 points for white pepper (Table 1). The composite price of black pepper decreased by 12.27% to US$ 3,216 per Mt from US$ 3,663 in February 2018 and for white pepper decreased by 6.6% from US$ 5,287 per Mt in February 2018 to US$ 4,939 in March 2018 (Table2). The decrease was mainly influenced by the significant decrease of FOB price in Viet Nam, the largest pepper exporting country. Price decrease was also recorded in other producing countries.

Table 1: IPC Price Index (Base Year: Average 2011 - 2015)

Note: The price index is calculated based on price developments in 2011-2015

Table 2: Composite Price of Black and White Pepper (US$/MT)

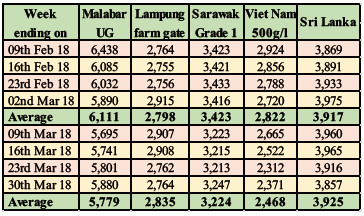

In March 2018, pepper price at all producing countries decreased, both for black and white pepper. Significant price decrease was recorded in Viet Nam by 13-14%. In India, Brazil and Sarawak the price of black pepper decreased by 5%; while in Lampung the price was relatively stable.

Table 3: Local price of black pepper in producing countries in US$/Mt

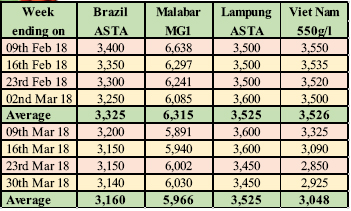

Table 4: FOB price of black pepper in producing countries in US$/Mt

HIGHLIGHT ON BRAZIL

AREA AND PRODUCTION

Brazil is the most important pepper producing countries in South America. In the last decade production of pepper in Brazil was around 40,000 Mt annually. In 2017 however the production increased significantly to around 60,000 Mt. Para state in northern part of Brazil is the main source of pepper in the country, contributes around 65-70% and the balance is resulted from the state of Espirito Santo in southern of Brazil. Peak harvesting season in Para is during August-October, while in Espirito Santo from January-March.

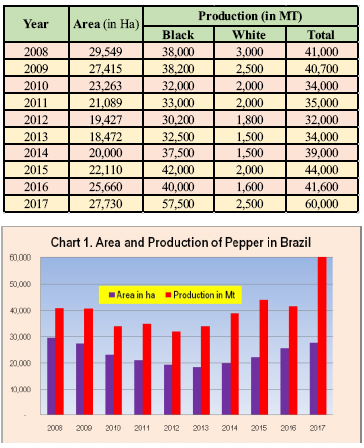

Area of pepper in Brazil has experienced a significant reduction in the year 2000s from 50,000 hectare in 2003 to 19-18,000 hectares in 2012-13. This was due to very low price prevailed during that period. Correspondingly production of pepper also decreased from 50,000 Mt in 2003 to 32-34,000 Mt in 2012-13.

Encouraged by significant price increase during 2010-2015, farmers in Brazil started replanting their gardens with pepper and a massive expansion has taken place since 2014. Farmers in Espirito Santo converted less productive coffee plants with pepper. Total area of pepper in 2017 is estimated to have reached 27,700 hectares. As a result of the expansion and intensive cultivation taken place in the previous few years and also supported by very good weather condition as well as the new pepper plants have reach full productive, production of pepper in 2017 increased substantially by 45% from 41,600 Mt to 60,000 Mt. Out of the total production in 2017, a volume of around 2,500 Mt is estimated as white pepper. Production in Espirito Santo increased significantly from around 15,000 Mt to 25,000 Mt, contributing more than 40% to the national production. In Para, the production also increased to around 35,000 Mt. In percentage however, contribution share of Para decreased to around 60%. With the increased production in Espirito Santo, Brazil has sufficient material for export throughout the year.

In 2017 was unlike with the situation in 2016, where real production of pepper decreased to 41,600 Mt from 44,000 Mt in 2015. The decrease was confirmed by significant decrease in export realized from 38,000 Mt in 2015 to 31,100 Mt in 2016. The decrease was due to severe weather factor, although new pepper plants have started fruiting.

In 2018 production of pepper in Brazil is estimated to remain high. Official source in Brazil (ABEP) however reported that production in 2018 would be slightly lower. The reason is less investment in the garden as a result of the low prices and death rate is estimated to be higher. Some sources reported that due to current low prices farmers even has switched pepper back to coffee and other commodities, such as cocoa and papaya. The following table and chart will clearly illustrate the development of area and production in Brazil over the last ten years.

Table 5: Are and Production of Pepper in Brazil

IMPORT AND EXPORT

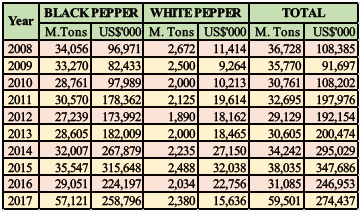

Supported by good harvest in 2017, export in 2017 experienced a substantial increase of 28,400 Mt (91%) to 59,500 Mt as against 31,100 Mt in 2016. In terms of value, Brazil realized export earning from pepper of around US$ 274 million in 2017 as against US$ 247 million in 2016, an increase of around 11%. Export in 2017 recorded the highest achieved by Brazil. In the past export of Brazil was between 30-40,000 Mt even lower.

Pepper traded in Brazil was mostly black pepper. Around five percent of the total export, even less was white pepper. Price of white pepper in Brazil was almost 50% higher than black. Export development in the last ten years is given below.

Table 6: Export of Pepper from Brazil during 2008-2017

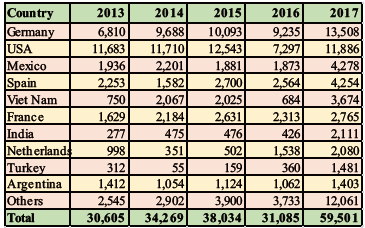

Brazilian pepper was mostly transported to Europe and American countries. Germany and United States of America continued was the main market for Brazil, together absorbing 42% of total export of Brazil. Germany imported 13,508 Mt (23%) and USA 11,886 Mt (20%). Mexico and Spain imported around 4,260 Mt (7%) each of pepper from Brazil in 2017. As a largest pepper producing countries, Viet Nam also imported significant quantity of 3,675 Mt from Brazil in 2017. Statistics of pepper export from Brazil by country is given below.

Table 7: Export of pepper from Brazil by country of destination in Mt

Beside exports, Brazil also imported pepper for internal use. Around 300-400 Mt was imported annually. In 2017 import of Brazil was 360 Mt, mainly ground pepper from India and Viet Nam.

Taking into account of reported stock at around 21,000 Mt in the beginning of 2017, production 60,000, import 300 Mt, 7,000 Mt for domestic consumption and 59,500 Mt of export, carryover for 2018 would be 14,800 Mt, lower from beginning stock in early 2017. Since Espirito Santo harvesting a good crop in the first quarter, Brazil is reported to have shown much less interest in carrying stocks forward.

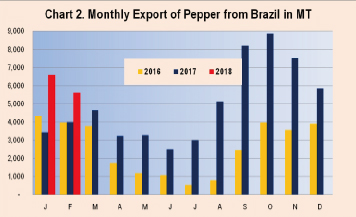

In 2018 export of pepper from Brazil is estimated to remain high. During January - February 2018 Brazil has exported 12,210 Mt valued at US$41.8 million as against 7,360 Mt over the same period last year. In quantity the export showed a significant increase by 4,850 Mt (66%). The export increase in the first two month was possible, supported by sufficient stock carried out from last year harvest. In February however, the export has shown a decreasing trend, although pepper harvest in Espirito Santo in early this year was on the full swing. This indicated output of this year harvest may not as good as projected earlier.

The following chart will illustrate monthly export development during 2016-2018 February.

PEPPER PRICE

Other than Viet Nam, production and export of pepper in Brazil also increased significantly in 2017. Brazil and Viet Nam together occupied more than 70% of world pepper export. Any development in these two countries will mainly affect global market. As a result of the above development, pepper price decreased significantly in the last two years. In March 2018 pepper price in Brazil continue to fall. In addition to the global trend, pepper harvest in Espirito Santo recently has also put pressure in the market.

In Brazil, almost all pepper traded in the country is black pepper. Only marginal quantity is white pepper. Pepper price reported in Brazil is having reference to black pepper. Trade source in Brazil (Coreimex) reported that pepper price in 2017 decreased significantly from US$ 6,953 per Mt to US$ 3,478 in December 2017, recording around 50% of the price has lost during the year. The price then decreased further to US$ 3.16 in March 2018, a decrease of around US$ 160 per Mt from price prevailed in February 2018 and decreased by US$ 2,860 per Mt from March 2017. Observing severe price decrease in 2017, it is understood that farmers not encouraging maintains the garden. As a result, production in 2018 may not increase, even decrease.

Some sources reported that production of pepper in most producing countries is estimated to remain high. However, under condition of low price, farmers are not interested for investment in the garden and lost spirit to maintain pepper plants. Consequently death rate is increasing. As a result of the situation expected better harvest for the upcoming crop season may not realized. The price may fluctuate in a narrow range for some times and will increase after finding a new equilibrium of supply and demand.

Table 8: Monthly Price of Black pepper in Brazil in US$/MT

Previous Publications

- MARKET REVIEW DECEMBER 2025

- MARKET REVIEW NOVEMBER 2025

- MARKET REVIEW OCTOBER 2025

- MARKET REVIEW SEPTEMBER 2025

- MARKET REVIEW - AUGUST 2025

- MARKET REVIEW - JULY 2025

- MARKET REVIEW - JUNE 2025

- MARKET REVIEW - MAY 2025

- MARKET REVIEW - APRIL 2025

- MARKET REVIEW - MARCH 2025

- MARKET REVIEW - FEBRUARY 2025

- MARKET REVIEW - JANUARY 2025

- MARKET REVIEW - DECEMBER 2024

- MARKET REVIEW - NOVEMBER 2024

- MARKET REVIEW - OCTOBER 2024

- MARKET REVIEW - SEPTEMBER 2024

- MARKET REVIEW - AUGUST 2024

- MARKET REVIEW - JULY 2024

- MARKET REVIEW - JUNE 2024

- MARKET REVIEW - MAY 2024

- MARKET REVIEW - APRIL 2024

- MARKET REVIEW - MARCH 2024

- MARKET REVIEW - FEBRUARY 2024

- MARKET REVIEW - JANUARY 2024

- MARKET REVIEW - DECEMBER 2023