a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Monthly Publication

Market Review - July 2018

Entering second semester of 2018, the market continued to show a decreasing trend. Price at all origins decreased up to 10 %, particularly in India, Viet Nam and Sri Lanka. In Indonesia and Sarawak, the decreases were at lower rate.

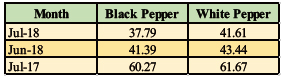

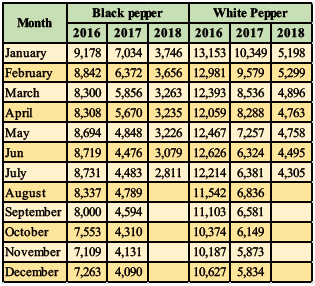

Pepper Price Index in July decreased by 3.6 points for black pepper and 1.83 points for white pepper from 41.39 and 43.44 respectively in June 2018 (Table 1). The composite price of black pepper decreased by 8.7% to US$ 2,811 per MT from US$ 3,079 in June 2018; while that of white pepper decreased by 4.2% from US$ 4,495 per MT in June 2018 to US$ 4,305 in July 2018 (Table2). Decreased price in Viet Nam the first largest pepper supplier have influenced significantly on the formation of composite price index in July 2017.

Table 1. IPC Price Index in US$/MT (Base Year: Average 2011 - 2015)

Note: The price index is calculated based on price developments during 2011-2015

Table 2: Composite Price of Black and White Pepper in US$/MT

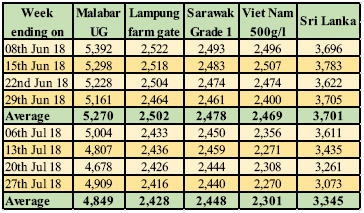

In July 2018, the market continued to show a decreasing trend. Price at all origins decreased, particularly in India, Sri Lanka and Viet Nam. In Indonesia and Sarawak, the price also decreased at relatively small.

As noticed that Viet Nam is predominantly the largest pepper supplier become the lead in making market direction. Price movement in Viet Nam will influence market direction in other countries. During July 2018, pepper price in Vietnam decreased by 7% for black and 9% for white pepper locally; while for fob price the decrease even reached 10%. Similar situation is also recorded in India. This is reflected that material in these countries from this year harvest still heavy. In Sri Lanka the price is mostly influenced by price development occurred in India, the main market for Sri Lankan pepper.

Unlike with the situation in Indonesia, although harvest in the country takes place in July/August, price decrease in Lampung and Bangka during July 2018 was relatively small, only 3%. Less output from current harvest and limited inventory carried from last year harvest is the main reason for this. As already reported earlier, production of pepper in Indonesia, particularly in Lampung is anticipated to be significantly less, due too many rains and low price prevailed since last year. Flowering and fruiting cannot come out perfectly during the season. Minimum input and maintenance applied in the garden has also contributed to the decrease in production.

Appearance of a few good gardens in north Lampung

Less maintenance is prominent situation in Bangka

Table 3: Domestic price of black pepper in US$/Mt

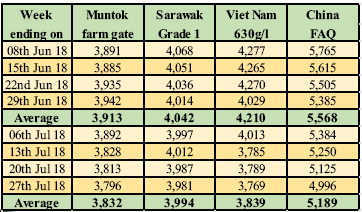

Table 4: Domestic price of black pepper in US$/Mt

Highlighted on Pepper Trade in the first half 2018.

World production of pepper during the last three years increased significantly from an average of 350,000 Mt in 2010-2014 to around 450,000 Mt in 2015-2017. Substantial increase occurred in 2017, where production of pepper has touched 500.000 Mt. This production level was substantially higher when compared to production level in 2016 at 429,000 Mt and 416,000 Mt in 2015. This achievement was largely because of the substantial increase of pepper production in Viet Nam and Brazil.

In line with the significant increase in production, export of pepper has also experienced a significant increase in the last three years. Substantial increase occurred in 2017 by 20% from 320,000 Mt in 2016 to 384,000 Mt in 2017. Out of this Viet Nam supplied 215,000 Mt (56%) in 2015. This was the main reason for significant fall of the price.

In 2018 pepper supply is estimated to remain high as a result of massive area expansion taken place in the previous years. Some source reported that production of pepper in Viet Nam and Brazil would be good this year, but official source estimated less. Official source in India and Indonesia projected production in 2018 would be better. Considering low prevailing price during 2017 till 2018, farm input and maintenance applied in the garden was minimal and this will definitely impact the output. Given sufficient inventory carried forward from last year harvest, export of pepper for 2018 is estimated to remain high, as reflected by export performance of the six main producing countries (Viet Nam, Brazil, Indonesia, India, Malaysia and Sri Lanka).

During January - June 2018 export of pepper from the above six major exporting countries was 198,000 Mt (172,000 Mt of black and 26,000 Mt of white pepper), registering an increase of 8% when compared to the export of 183,000 Mt in the corresponding period last year. Exports from Vietnam, Brazil and Indonesia increased, while from India and Sri Lanka decreased. Export from Malaysia was more or less same. Black pepper export increased by 8% and for white pepper increased by 11%.

Considering anticipated less output in 2018, export in the second semester this year is estimated to be lower when compared to export in the second semester last year.

The following chart will illustrate the development of export of the six major exporting countries during January - June 2018 and January - June 2017.

During the first half of the year, Viet Nam the largest supplier has shipped 132,150 Mt, increased by 5% from 125,360 Mt in the same period last year. Brazil's export increased by 10,000 Mt from 21,000 Mt in January - June 2017 to 31,000 Mt in the first six months this year. The significant increase was sourced from big supply carry forward from last year harvest taken place in September-October last year. Pepper harvest in early 2018 in Espirito Santo has also contributed to the high supply in the first half of the year.

Marginal increase of 1% (200 Mt) is recorded for Indonesia's export from 18,200 Mt during January - June 2017. Export of black pepper decreased by 2,900 Mt; while for white pepper increased by 2,100 Mt.

Export of India and Sri Lanka decreased by 6% and 29% to only 8,800 Mt and 3,000 Mt respectively during January - June 2018 as against 9,300 Mt and 4,200 Mt in the same period last year. Export of pepper from Malaysia during January - June 2018 was more or less same as last year at around 5,000 Mt.

In the first half of the year Brazil has increased their share in world market of pepper by aggressive selling. Among the six exporting countries, only Brazil successfully increases its share to 16% from 11% last year. Although decrease by 2% Viet Nam continued to be the largest supplier, occupying 67% of the market during the first half of 2018.

Tentative export figures of the six major exporting countries and their shares during January - June in the year 2017-2018 are given below:

Table 5: Export of black pepper June 2017-June 2018 in Mt

Note: Figures are provisional and subject to revision.

Previous Publications

- MARKET REVIEW - NOVEMBER 2023

- MARKET REVIEW - OCTOBER 2023

- MARKET REVIEW - SEPTEMBER 2023

- MARKET REVIEW - AUGUST 2023

- MARKET REVIEW - JULY 2023

- MARKET REVIEW - JUNE 2023

- MARKET REVIEW - MAY 2023

- MARKET REVIEW - APRIL 2023

- MARKET REVIEW - MARCH 2023

- MARKET REVIEW - FEBRUARY 2023

- MARKET REVIEW - JANUARY 2023

- MARKET REVIEW - DECEMBER 2022

- MARKET REVIEW - NOVEMBER 2022

- MARKET REVIEW - OCTOBER 2022

- MARKET REVIEW - SEPTEMBER 2022

- MARKET REVIEW - AUGUST 2022

- MARKET REVIEW - July 2022

- MARKET REVIEW - June 2022

- MARKET REVIEW - MAY 2022

- MARKET REVIEW - APRIL 2022

- MARKET REVIEW - March 2022

- MARKET REVIEW - February 2022

- MARKET REVIEW - January 2022

- MARKET REVIEW - December 2021

- MARKET REVIEW - November 2021