a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Quarterly Publication

1<sup>st</sup> Quarterly 2019 Report

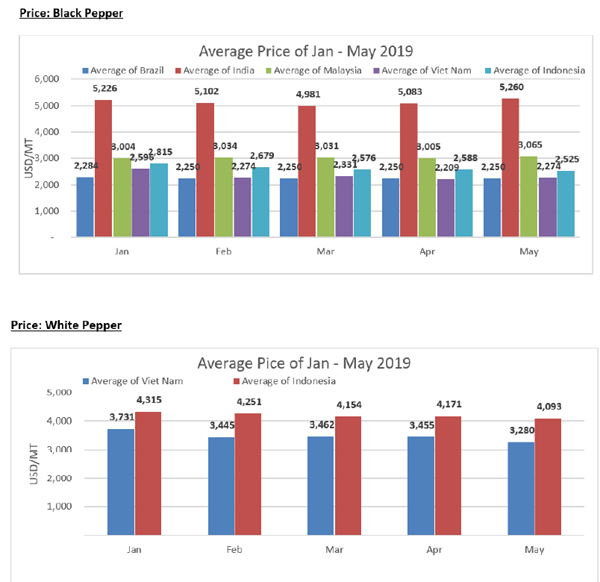

2019 apparently is a stable year as compared to the past few years particularly from 2015 to 2017, during which the prices fell sharply. Fob Prices of Viet Nam black pepper 570 g/l peaked at USD 9000/MT in 2015 and today stand in the vicinity of 2300.

Supply Situation:

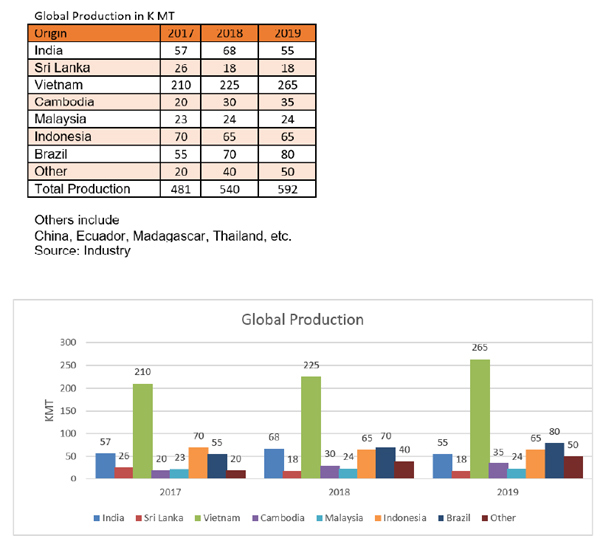

Weather of 2018 was conducive for pepper farming and backed by the planting in the past few years the global crop of 2019 is expected to be good. Starting with India and Viet Nam the Pepper flows were decent and the origin that deserves the most attention is Brazil. The 2018 Crop flows into 2019 were higher than most previous years. At present there is close to 15% more supply than the expected demand. The prices have accounted for the excess supply much ahead in time and therefore they are stable in the 2019 as compared to previous years. With prices close to or below cost of production in some cases farmers are adopting suboptimal farming practices cutting costs where every possible. Going into 2020 initial surveys depict that farmer sentiment, weather in 2019 are not as conducive and this may lead to pressure on the supply side due to reduction in new crop yields.

Demand Side:

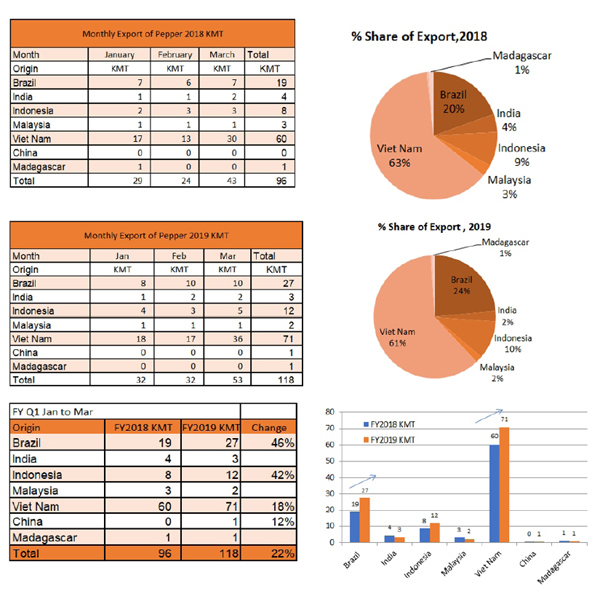

Shipments: Due to lower prices we observe that industry starts to fill up pipelines fearing an upward movement after prices reaches decade low levels. In Q1 the industry imported close to 22% more pepper from the origins when compared to the same period last year.

Viet Nam, Brazil and Indonesia put together constitute close to 95% of the global export from the origins. In FY Q1 2019 all three origins exported much more than previous year same period. Brazil and Indonesia shipments increased by 40% while Viet Nam recorded a jump of 18%. The global demand is slated to grow not more than 2-3%. Asian countries have been the key drivers of growth in FY 2019 as they imported Brazilian pepper which was not a traditional origin for them.

Salient Points:

1. Global Pepper prices are at a decade low.

2. Industry starts to fill in pipelines, purchase forward and buy more due to an attractive price.

3. Industry participants expect drop in yields in 2020 due to weather and low farmer morale as prices come close to cost of production.

Previous Publications

- GLOBAL PEPPER MARKET REPORT ANNUAL REVIEW 2025 AND OUTLOOK 2026

- Global Pepper Report - First Half January to June FY 2025

- GLOBAL PEPPER INDUSTRY SEMESTERLY REPORT

- GLOBAL PEPPER INDUSTRY 3RD QUARTERLY REPORT (JULY - OCTOBER 2022)

- WORLD PEPPER INDUSTRY 2ND QUARTERLY REPORT (JAN -JUNE 2022)

- 1st Quarterly 2022 Report

- 3rd Quarterly 2021 Report

- 2nd Quarterly 2021 Report

- 1st Quarterly 2021 Report

- 4th Quarterly 2020 Report

- 3rd Quarterly 2020 Report

- 2nd Quarterly 2020 Report

- 1st Quarterly 2020 Report

- 4th Quarterly 2019 Report

- 3rd Quarterly 2019 Report

- 2<sup>nd</sup> Quarterly 2019 Report

- 1<sup>st</sup> Quarterly 2019 Report