a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Quarterly Publication

2nd Quarterly 2020 Report

Pepper FY2020 Q2 Report

Global Coverage

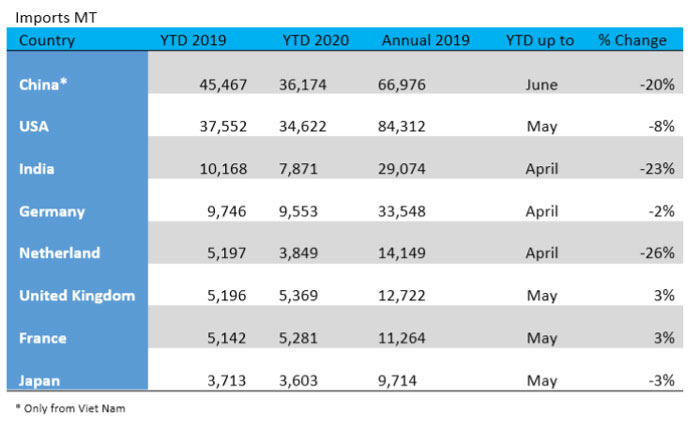

In 2019 Importing countries globally purchased a large quantity filling their pipelines at decade cheap prices. With expectations of a slight dip in supply during 2020 buying was done for forward months. Then came Covid-19 and imports into China dipped due to both logistical disruptions and dip in demand especially on the food service side. Above table depicts a drop in offtake from Vietnam in FY 2020.

USA and EU on the other hand bought a bit extra to put cargo on water fearing Vietnam may go in lockdown. Vietnam was open for all practical reasons and shipments were done in time. The biggest drop in import other than China were in India and USA. Both countries imported closed to 10% less during this period. Some part of import was substituted by cargo from Brazil. There was a significant drop in Netherlands during the same period.

Global Import YTD same period has dropped from 10-15%. Farmers and Traders in origins have become bullish after they saw a price rise with the advent of China in May and June. With no demand from other regions prices in Vietnam have corrected by 15% from their peak. Harvests in Indonesia and Brazil is what all parties continue to watch carefully.

We believe coverage at destinations continues to be healthy.

Export Shipments

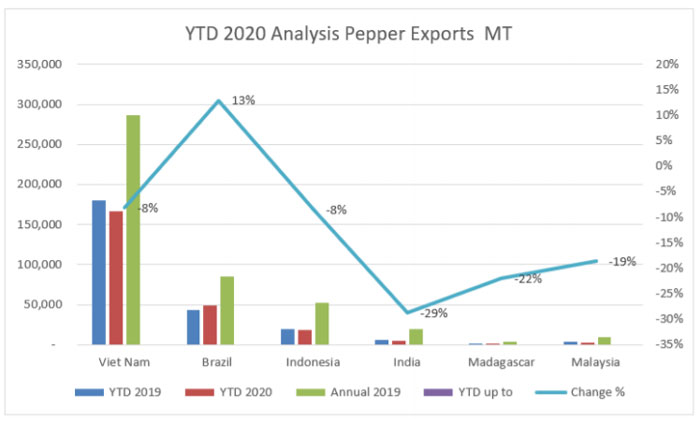

There has been a drop in exports for the First Half of 2020 and this was expected due to lock downs at destinations, dip in demand and heavy pipeline stock at the destination coming through from 2019.

India saw the sharpest decline in exports of 29%. This was mostly due to imports for re-exports could not be done. Some business went to Vietnam in terms of processed cargo such as steam sterilized and ground pepper. Despite this a huge drop in Chinese imports from Vietnam dragged the overall number to a drop of 8% when one looks at exports from Vietnam. Brazil was the only origin with rise in exports due to the advent of non-traditional markets.

In the First Half other than Brazil all origins have shipped lesser as compared to the same period last year. We feel inventories at farmgate are decent to cover for the balance period of the year despite a lower crop projected this year.

Vietnam Blossom

We expect a normal blossom despite a less conducive weather. The key concern is the reducing area under plantation as farmers invest less in farming and chose to plant other viable options like fruits and vegetables.

Indonesia Harvest

Lampung (Black Pepper)

Though Black Pepper harvest in Lampung is expected to peak in August, the crop for 2020 is projected to decrease as compared to last years as most regions aside from North Lampung reported to expect less crop this year due to pest and diseases as occurrence of foot root diseases were spotted at Tanggamus and East Lampung. Furthermore, farmers also attested that last year prolonged dry season had worsened the condition of this year's crops.

Bangka Belitung (White Pepper)

Every regions of the Bangka Belitung reporting that Muntok White Pepper crop this year is expected to experience a significant decreasing trend when compared to 2019. Farmers unable to cope with the production cost which exceed the price of white pepper as well as being burden with the pest and disease problem of the crop due to lack of maintenance. As like in Lampung the condition of the fruits

in Bangka Belitung was worsened because of the prolonged dry season last years which is more harmful towards white pepper plantation.

Previous Publications

- GLOBAL PEPPER MARKET REPORT ANNUAL REVIEW 2025 AND OUTLOOK 2026

- Global Pepper Report - First Half January to June FY 2025

- GLOBAL PEPPER INDUSTRY SEMESTERLY REPORT

- GLOBAL PEPPER INDUSTRY 3RD QUARTERLY REPORT (JULY - OCTOBER 2022)

- WORLD PEPPER INDUSTRY 2ND QUARTERLY REPORT (JAN -JUNE 2022)

- 1st Quarterly 2022 Report

- 3rd Quarterly 2021 Report

- 2nd Quarterly 2021 Report

- 1st Quarterly 2021 Report

- 4th Quarterly 2020 Report

- 3rd Quarterly 2020 Report

- 2nd Quarterly 2020 Report

- 1st Quarterly 2020 Report

- 4th Quarterly 2019 Report

- 3rd Quarterly 2019 Report

- 2<sup>nd</sup> Quarterly 2019 Report

- 1<sup>st</sup> Quarterly 2019 Report