a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Quarterly Publication

3rd Quarterly 2020 Report

Vietnam:

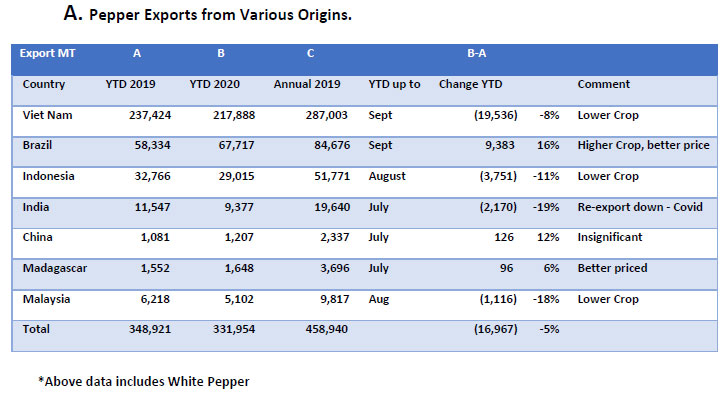

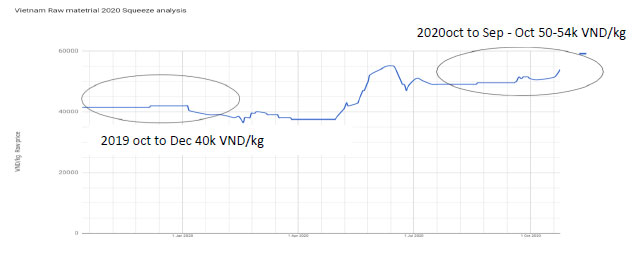

YTD 2020 despite being affected by Covid-19 was a good year in terms of Exports. The shipments from Vietnam from Jan to Sep or the first 9 months were down by 8%. The biggest fall in exports came from imports drop from China at 8,000 MT out of the total drop of 19,536 MT. The crop in Vietnam was short by 10% i.e. 25,000 MT and considering that many countries bought a little but more towards the end of 2019 for shipment in 2020, their offtake in 2020 was therefore marginally lower. Overall, the shipments and crop availability from Vietnam have been balanced. This kept prices stable till the first half of the year. As soon as China came back to market, the prices rose as supply was just in balance to demand and therefore any sudden spike in buying led to increase in price followed by a steady drop to stabilized at 50,000 VND/Kg of raw material.

Note: Once prices rise the markets also wait and ability to stock at higher prices also reduces due to working capital constraints.

Brazil:

A good crop in Brazil coupled with lower prices towards end of 2019 and beginning of 2020 made this origin as a good alternative to Vietnam. Especially the sundried pepper gained importance due to its lower incidence of pesticides.

Brazil exported a record 67,000 MT in the first 9 months. This also explains that Brazil has shipped almost 10% more material this year in the first 9 months. Therefore, inventory levels are not high and with news of an impending the prices of Brazilian ASTA have shot up. The arbitrage of 20% in 2019 has come down to just 5% currently and therefore slowly one may see customers coming back to Vietnam in the new season. Brazil has been following prices of Vietnam closely and we expect it to remain at a lower discount than in the past. With El Nina, harvest in Vietnam could get delayed and therefore the chances of prices coming down in the backdrop of a lower inventory seems difficult.

Indonesia:

Seems to be on track with small drop in exports as White crop was not great and the prices in this origin did not come down. We believe Indonesia will catch up in the last quarter of 2020 as now we are seeing Indonesia to be priced competitively. Exports from Indonesia to Vietnam and China may rise beyond normal in the last quarter as Vietnam and Brazilian prices have now soared past Indonesia.

India:

Covid-19 led shutdowns have impacted processors in India who were importing pepper and re-exporting the same to various locations. This has led to a drop in exports from India.

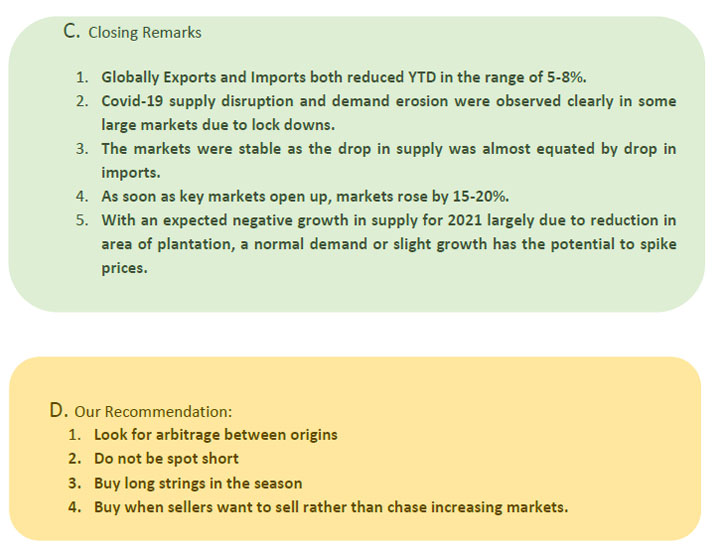

Overall YTD 2020 declined 5% in shipments from various origins put together. One can attribute this to lower supply, lesser demand by Covid-19 and a price rise towards the second half. Despite lower global offtake prices have risen signals a strong message that origins are not under pressure to sell and are comfortable with their inventory levels thereby prices could remain stable to firm till the new crop flows in 2021.

While Data for all markets is not on the same time scale, YTD comparison for the same months gives us a fair idea of what is happening in these markets.

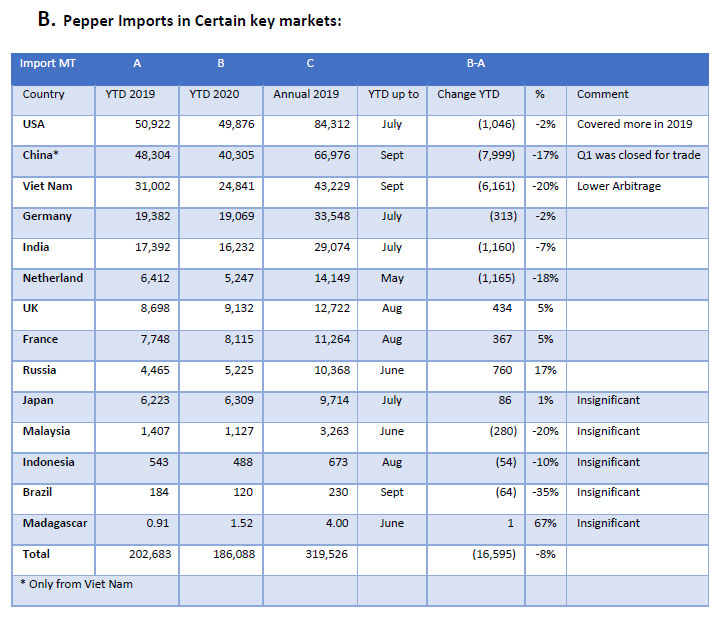

The top 5 importers - USA, China, Vietnam (re export), Germany, India (re export) gives us a pulse of the trade.

USA:

A drop in 2% is in line with Global slowdown of GDP and perhaps the key factor here is that shipments have not grown so volumes can rise by 5% from this base once things normalize.

China:

A drop of 8,000 MT, largely a short fall of imports from Vietnam due to border closers. 2021 we expect these volumes to come back even if markets remain flat and do not grow.

Germany:

Also, in line with the drop in USA of 2%. The largest consuming nations of the world with open borders for imports witnessed a decline of 2%. Had things been normal perhaps they would have grown by 2-3%. So, this we can say that offtake has been lower than usual expectation.

Vietnam and India:

Both are importing for processing and re-export. While Vietnam imported less as one sees a lower arbitrage with Brazil, Indian imports reduced due to Covid-19 and border closures leading to supply disruptions. Brazil exports almost 30% went to Vietnam. The volumes exported to Vietnam were lower, but Brazil's total exports were higher manifesting that Brazil did direct exports to many destinations and also replaced Vietnam in non-traditional markets such as the middle east.

Previous Publications

- GLOBAL PEPPER MARKET REPORT ANNUAL REVIEW 2025 AND OUTLOOK 2026

- Global Pepper Report - First Half January to June FY 2025

- GLOBAL PEPPER INDUSTRY SEMESTERLY REPORT

- GLOBAL PEPPER INDUSTRY 3RD QUARTERLY REPORT (JULY - OCTOBER 2022)

- WORLD PEPPER INDUSTRY 2ND QUARTERLY REPORT (JAN -JUNE 2022)

- 1st Quarterly 2022 Report

- 3rd Quarterly 2021 Report

- 2nd Quarterly 2021 Report

- 1st Quarterly 2021 Report

- 4th Quarterly 2020 Report

- 3rd Quarterly 2020 Report

- 2nd Quarterly 2020 Report

- 1st Quarterly 2020 Report

- 4th Quarterly 2019 Report

- 3rd Quarterly 2019 Report

- 2<sup>nd</sup> Quarterly 2019 Report

- 1<sup>st</sup> Quarterly 2019 Report