a UNESCAP Intergovermental Organization

a UNESCAP Intergovermental Organization

Quarterly Publication

GLOBAL PEPPER MARKET REPORT ANNUAL REVIEW 2025 AND OUTLOOK 2026

Executive Summary

The global pepper market in 2025 continued to operate under structurally tight conditions, characterized by limited carry-over stocks and rising production, compliance, and logistics costs. While partial supply recovery was observed in select origins, most notably Brazil and Malaysia, these improvements were insufficient to fully offset persistent constraints in key Asian producing countries, particularly Vietnam, India, and Indonesia.

On the demand side, consumption remained resilient across major markets, led by Asia and the Middle East, with a growing preference for traceable, compliant, and sustainably produced pepper. This shift has reinforced differentiation within the market, increasingly favoring origins and supply chains able to meet evolving regulatory and quality requirements.

Supported by low inventory levels and constrained exportable surpluses, global pepper prices remained firm throughout 2025. Brazil's increasing role as a reliable and competitively priced supplier has contributed to setting an effective price floor in international trade, while price volatility continued to reflect sensitivity to weather patterns, compliance costs, and broader macroeconomic developments.

Looking ahead to 2026, the global pepper market is expected to remain structurally tight. While overall production levels are projected to remain broadly stable, limited stock buffers and continued exposure to climatic and regulatory risks suggest a firm to moderately bullish price environment. Market conditions are therefore likely to remain sensitive to supply disruptions, reinforcing the importance of transparency, compliance, and coordinated market intelligence across the global pepper value chain.

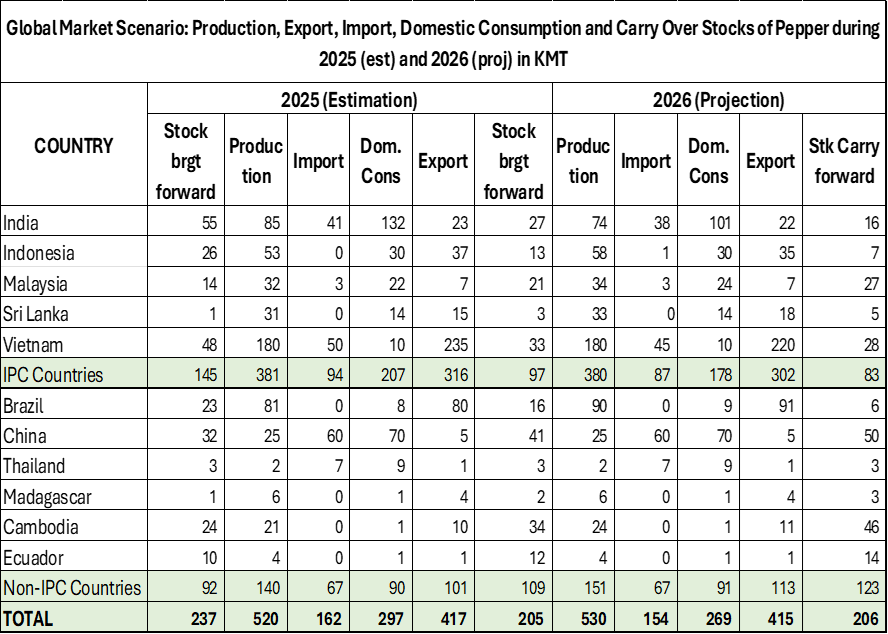

Source: IPC Estimation, Figures have been discussed at the 53rd Annual Session and Meetings of the International Pepper Community

2. Global Supply Overview and Carry-Over Stocks

Global pepper supply continues to be concentrated among a limited number of producing countries, with Vietnam, Brazil, India, Indonesia, and Malaysia accounting for the majority of global output and exports. In contrast, consumption remains widely distributed across Asia, Europe, the Middle East, and the Americas, reinforcing the structural sensitivity of the market to production developments in a small number of origins.

Entering 2026, global carry-over stocks are estimated at approximately 205 KMT, underscoring the continued tightness of the market despite a projected increase in total production to around 530 KMT. Within IPC member countries, carry-over stocks are estimated at only 97 KMT, a sharp decline from 145 KMT recorded a year earlier. Stock tightness is particularly evident in Vietnam and India, reflecting sustained export outflows in the former and strong domestic absorption in the latter.

Vietnam's carry-over stocks are estimated to have declined to 33 KMT, largely due to strong shipment activity throughout 2025. India's stocks are projected at 27 KMT, constrained by high domestic consumption levels and limited production recovery. These developments have reduced buffer capacity in two of the world's most influential pepper origins.

Brazil presents a distinct supply profile. Despite improved production, carry-over stocks are projected to decline from 23 KMT at the beginning of 2025 to 16 KMT entering 2026. This reflects Brazil's role as a flow-through export origin, where production gains are rapidly absorbed by international demand rather than accumulated as inventories. As a result, Brazil has increasingly emerged as a key reference point for price formation rather than a source of surplus stocks.

Non-IPC countries collectively account for an estimated 109 KMT of carry-over stocks. However, a significant portion of these volumes is held in consumption-oriented markets, particularly China (approximately 40 KMT), which limits their immediate availability to the export market.

Key Observations

- With the exception of Brazil, most major producing origins are projected to experience flat to marginally lower production in 2026.

- Aggregate production among IPC member countries is expected to remain broadly stable at approximately 380 KMT.

- Global production, including non-IPC countries, is projected at around 530 KMT, broadly in line with 2025 levels.

- India has recorded the most pronounced production decline over the past two years, contributing to increased reliance on imports.

- Global carry-over stocks are projected to decline by approximately 30 KMT by the end of 2025 compared to early 2024, providing firm underlying support for prices entering 2026.

3. Supply Country-wise Analysis

Vietnam

Vietnam continues to be the world's largest producer and exporter of pepper, accounting for a substantial share of global trade. In recent years, however, production growth has moderated, reflecting a combination of prolonged dry spells, increasingly irregular rainfall patterns, and persistent disease pressure, particularly related to root rot and soil degradation.

Rising labour costs and the tightening of food safety and compliance requirements have contributed to higher production costs, while replanting activity remains relatively limited. At the same time, Vietnam has continued to strengthen its position in value-added processing, sustainability initiatives, and traceability systems, reinforcing its role across higher segments of the value chain.

2026 Outlook:

Pepper production in Vietnam is expected to remain broadly stable in 2026. However, exportable availability may remain constrained as quality differentiation, compliance requirements, and domestic utilization increasingly shape marketable volumes.

Brazil

Brazil represents a comparatively positive supply development heading into 2026. Favourable weather conditions and improvements in farm management practices have supported yield recovery, particularly in Espirito Santo and Bahia. These gains are underpinned by relatively high productivity levels and a competitive cost structure.

Brazil's harvest calendar, which allows for two main export windows, provides international buyers with a degree of flexibility and has enhanced the country's role in global trade flows. As production gains are rapidly absorbed by export demand, Brazilian offers have increasingly served as a key reference point in international price formation.

2026 Outlook:

Brazilian exports are projected to increase from approximately 80 KMT in 2025 to around 90 KMT in 2026. This is expected to reinforce Brazil's role as a stabilizing supply origin, contributing to price formation rather than generating surplus inventories.

India

India's pepper sector continues to operate under a set of long-standing structural constraints. Aging vines, limited replanting activity, and labour availability challenges have moderated production growth in recent years. At the same time, robust domestic consumption absorbs a substantial share of output, resulting in limited exportable availability.

In response to these dynamics, India has increasingly relied on imports to support processing and re-export activities. This evolution reflects a gradual shift in India's market role, from a predominantly export-oriented origin toward a more consumption- and value-addition-focused profile.

2026 Outlook:

India's domestic supply balance is expected to remain tight in 2026, with limited scope for a significant increase in export volumes. Import requirements are therefore likely to persist in support of downstream processing activities.

Indonesia

Indonesia remains a key supplier of white pepper in the global market. However, production recovery has progressed more gradually than previously anticipated, reflecting ongoing disease pressure, weather variability, and post-harvest quality management challenges.

National initiatives promoting Good Agricultural Practices (GAP), improved post-harvest handling, and enhanced traceability systems are ongoing. While these efforts are expected to strengthen Indonesia's supply position over the medium term, measurable impacts on volume and quality consistency will require sustained implementation.

2026 Outlook:

Indonesia is expected to maintain a stable supply profile in 2026, with limited near-term growth. Continued progress in quality management and compliance is likely to remain a key determinant of market positioning.

Malaysia

Malaysia, particularly the state of Sarawak, continues to position itself as a premium pepper origin. Although overall production volumes remain relatively modest, output has shown gradual growth supported by consistent quality standards, branding initiatives, and a strong emphasis on compliance.

Malaysia's supply profile is increasingly characterized by quality differentiation rather than volume expansion, reinforcing its niche role within the global pepper market.

2026 Outlook:

Malaysian production is expected to remain stable to slightly higher in 2026, with the country continuing to serve premium market segments rather than contributing to bulk supply growth.

Sri Lanka

Sri Lanka's pepper production continues to exhibit a high degree of variability, largely influenced by weather conditions, input availability, and broader farm-level constraints. As a result, output levels remain sensitive to short-term shocks, contributing to intermittent volatility rather than sustained growth in global supply.

2026 Outlook:

Sri Lanka is expected to maintain a variable but broadly stable supply profile in 2026. While volumes remain modest, developments in weather conditions and input access will continue to play a key role in shaping production outcomes.

Cambodia

Cambodia has demonstrated a steady growth trajectory in recent years, supported by relatively high yields per hectare and increasing integration into regional supply chains. Improvements in farm practices and market access have gradually strengthened Cambodia's position as a supplementary supply origin within the global pepper market.

2026 Outlook:

Cambodia is expected to continue its gradual growth path in 2026. While its contribution to global supply remains limited in scale, the country's role in supporting diversification of sourcing options is becoming increasingly relevant.

Taken together, developments across both major and emerging producing origins highlight a central feature of the global pepper market: supply remains concentrated, buffer stocks are limited, and sensitivity to climatic, regulatory, and cost-related factors is increasing. In this context, demand-side dynamics, including evolving consumption patterns, regulatory frameworks, and buyer preferences, are playing a progressively more influential role in shaping market outcomes.

Global Demand Analysis

Global demand for pepper in 2025 remained resilient across major consuming regions, underpinned by population growth, evolving consumption patterns, and the continued expansion of food processing industries. Asia continued to account for the largest share of global consumption, with China playing a central role, supported by its large domestic market and diversified import sourcing strategies.

Demand from the Middle East remained steady, characterized by consistent volume requirements and a high degree of price sensitivity. The region continues to serve as a key trading and redistribution hub, linking producing origins with end markets across West Asia and beyond.

In Europe, overall demand levels remained stable, increasingly shaped by regulatory requirements related to food safety, sustainability, and traceability. Compliance with maximum residue limits (MRLs), certification schemes, and quality assurance standards has become a decisive factor in market access, contributing to greater segmentation between compliant and non-compliant supply.

In the United States, tariff-free access continued to support long-term consumption trends, although buyer behaviour remained cautious amid broader macroeconomic uncertainty. Inventory management strategies and regulatory compliance considerations increasingly influenced purchasing decisions throughout 2025.

Across all regions, buyers are placing growing emphasis on:

- Steam-sterilized and value-added pepper products

- Sustainable and certified supply chains

- Traceable and regulatory-compliant origins

This structural shift in demand has reinforced market differentiation, with premium segments attracting more stable demand, while lower-grade and non-compliant products face increasing margin pressure.

5. Price Dynamics

Pepper prices throughout 2025 were underpinned by a combination of structurally low global inventories, rising production and compliance costs, and limited short-term supply flexibility across major origins. These conditions contributed to a generally firm price environment, despite periodic fluctuations observed during the year.

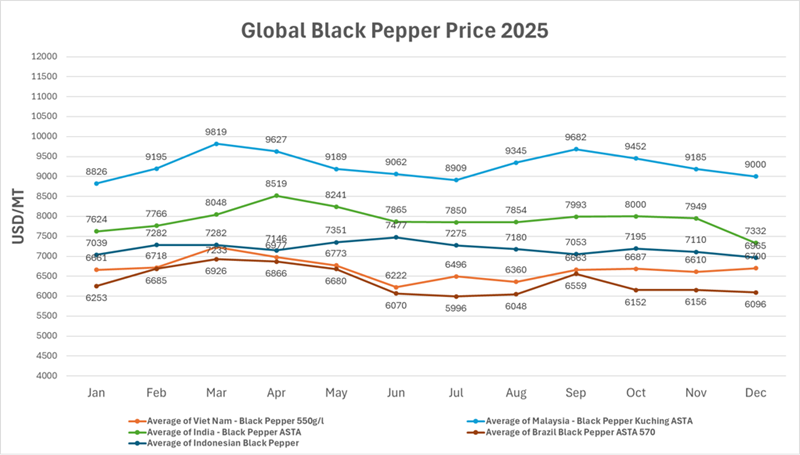

As illustrated in the Global Black Pepper Price 2025 chart, prices across major origins followed a broadly similar trajectory. Prices strengthened during the first quarter, reflecting tight availability ahead of peak harvest periods, before moderating in mid-year as seasonal supplies entered the market. From the third quarter onwards, prices stabilized at relatively elevated levels, supported by continued inventory tightness and steady demand. Among major origins, Brazilian black pepper prices consistently provided a reference range for the market, reflecting Brazil's role as a reliable flow-through supplier rather than a source of surplus stock accumulation.

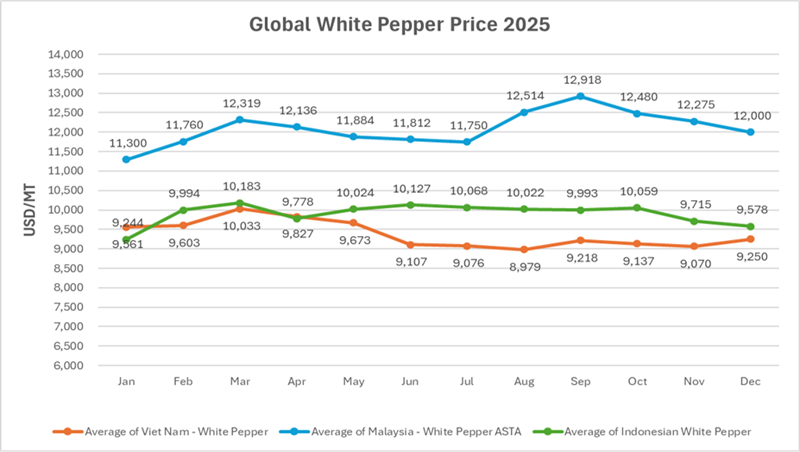

The Global White Pepper Price 2025 chart indicates a comparable pattern, albeit at a higher absolute price level, reflecting the more specialised nature of white pepper production and processing. Prices for white pepper remained relatively stable throughout the year, with less pronounced mid-year softening compared to black pepper. This stability was particularly evident for origins supplying compliant and quality-consistent products, underscoring the growing importance of post-harvest handling, processing standards, and traceability in price formation.

Across both black and white pepper markets, rising compliance-related costs, including those associated with maximum residue limits (MRLs), sustainability certification, and quality assurance, have become increasingly embedded within the overall cost structure. These factors have contributed to a higher structural price base, reducing the scope for sustained downward price adjustments even during periods of seasonal supply pressure.

Overall, price developments in 2025 highlight the market's increasing sensitivity to structural constraints rather than short-term cyclical movements alone. Price formation is progressively shaped by inventory positions, compliance capacity, and supply reliability, reinforcing the importance of transparency and quality differentiation across the global pepper value chain.

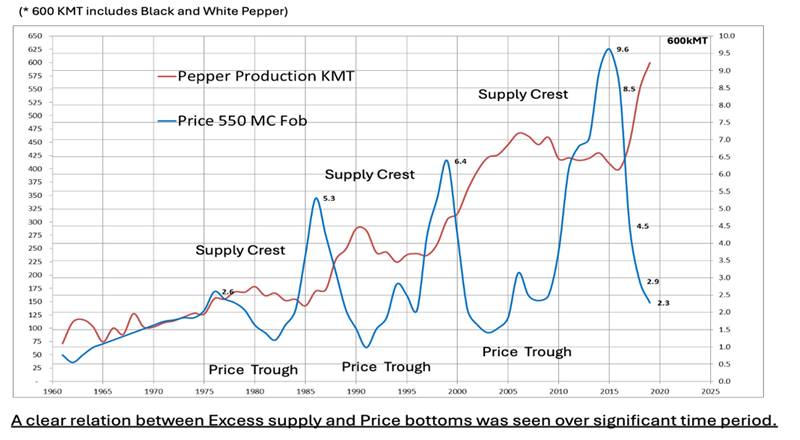

A. Price Movement: A Long-Term Perspective (1950-2020)

An examination of pepper price movements over the long term reveals a clear and recurring relationship between global supply dynamics and price behaviour. As illustrated in the chart, periods of sustained production expansion, often marked by successive increases in global output, have historically coincided with phases of price moderation or prolonged price troughs. Conversely, periods in which supply growth lagged demand have been associated with pronounced price upswings and the formation of price peaks.

The historical pattern highlights a cyclical interaction between production responses and market signals. Supply crests, typically following phases of strong price incentives, have tended to precede downward adjustments in prices as additional volumes enter the market. In contrast, when production growth slows or fails to keep pace with demand expansion, prices have demonstrated a tendency to reach new highs, reflecting constrained availability and tightening inventories.

While these long-term fundamentals continue to underpin price formation, the pace and amplitude of price movements have evolved. In recent decades, the increasing availability of real-time market information, driven by digital connectivity and rapid information dissemination, has contributed to greater short-term price responsiveness. As a result, market participants now react more quickly to changes in production expectations, weather events, and policy developments, amplifying short-term volatility within an otherwise structurally driven price cycle.

Overall, the long-term perspective underscores that while short-term fluctuations may be influenced by information flows and market sentiment, underlying supply-demand balances remain the principal determinant of pepper price trends over extended periods.

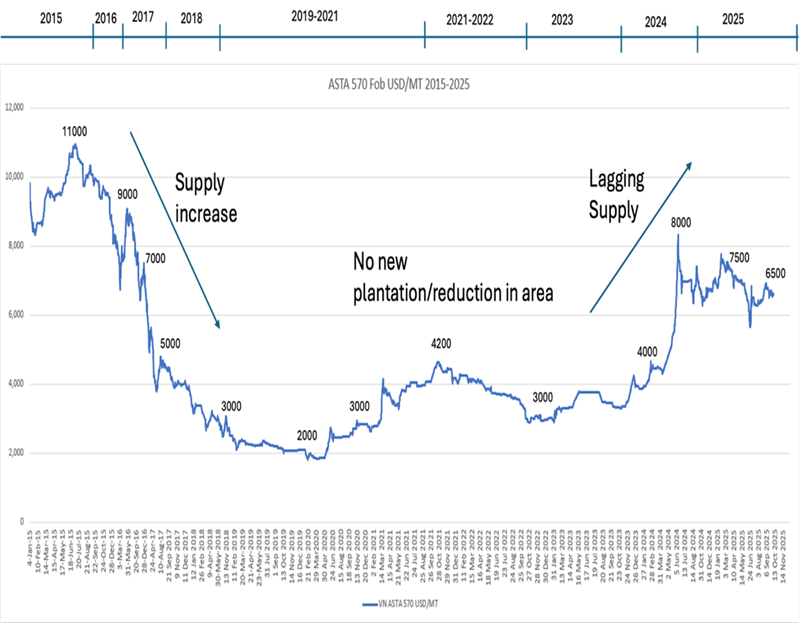

Black Pepper Price Movement in the Past Decade (2015 - 2025): Case Study of Vietnam ASTA 570 FOB

An examination of black pepper price movements over the past decade, using Vietnam ASTA 570 FOB as a reference, illustrates the interaction between supply responses, investment cycles, and delayed production adjustment.

Following a period of elevated prices during 2015-2016, global production expanded as higher returns incentivized planting and intensification. This response contributed to a sustained downward correction in prices between 2017 and 2019, with values declining sharply as additional volumes entered the market.

From 2019 onwards, price recovery remained gradual and uneven. Limited new plantation activity, combined with reductions in cultivated areas in certain origins, constrained supply growth. During this period, production responses lagged behind demand recovery, resulting in a prolonged phase of relatively low but stabilizing prices.

A more pronounced upward adjustment became evident from 2023 onwards, as cumulative supply constraints intersected with recovering demand. The absence of significant new planting over the preceding years reduced the market's ability to respond quickly to improved price signals, contributing to a sharper price escalation.

By 2024, prices rose markedly, reflecting lagging supply responses rather than short-term market disruptions. Although prices moderated somewhat in 2025, they remained well above historical averages, underscoring the structural nature of the current price environment.

Overall, the past decade highlights a recurring pattern in the pepper market: production responses to price signals are inherently delayed, and periods of underinvestment or area reduction tend to manifest in price volatility several years later. This dynamic reinforces the importance of forward-looking production planning and market transparency in mitigating extreme price cycles.

Building on the longer-term price dynamics observed over the past decade, developments in 2024-2025 reaffirm the central role of supply-demand fundamentals in shaping pepper price movements. While prices experienced a sharp upward adjustment in 2024, reflecting cumulative supply constraints, price behaviour in 2025 was characterized by heightened short-term volatility rather than a sustained directional trend.

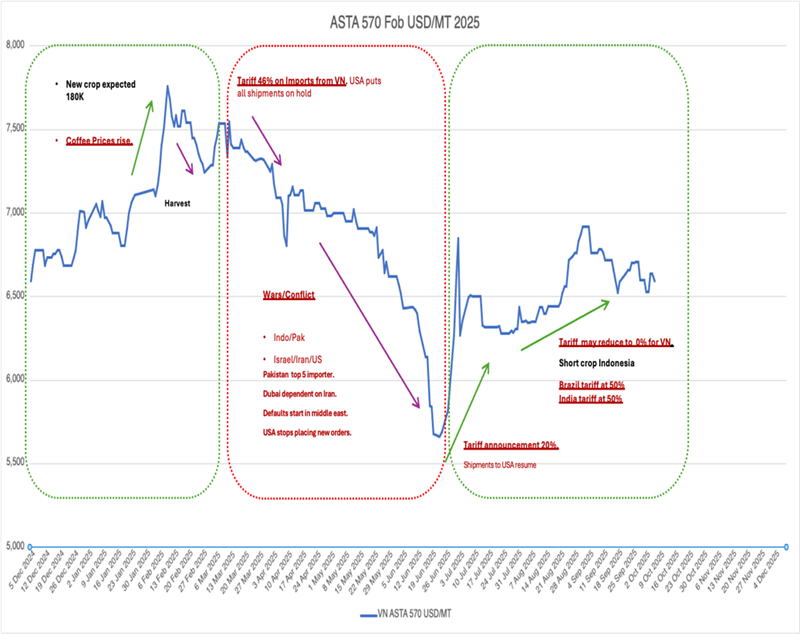

B. Short-Term Price Developments in 2025

At the beginning of 2025, pepper prices strengthened, reaching approximately USD 7,500 per metric ton, supported by expectations of tighter seasonal availability and broader movements in related agricultural commodity markets. As harvesting activity commenced toward the end of February, prices began to soften in line with seasonal supply inflows.

During March and April, market sentiment weakened further amid a combination of external developments that disrupted trade flows and buyer confidence. These included changes in trade policy affecting key importing markets, heightened geopolitical tensions in several consuming regions, and temporary interruptions to commercial activity in parts of South Asia and the Middle East.

Collectively, these developments contributed to short-term price corrections, delays in shipments, and increased caution among market participants. While these factors weighed on prices during the period, they did not fundamentally alter the underlying supply constraints identified earlier, underscoring the distinction between short-term market disruptions and longer-term structural dynamics.

Black Pepper Monthly Price Movement 2025: Case Study of Vietnam ASTA 570 FOB

An examination of monthly black pepper price movements in 2025, using Vietnam ASTA 570 FOB as a reference, highlights the pronounced short-term volatility experienced during the year and the sensitivity of prices to seasonal and external factors.

During the early months of 2025, prices strengthened steadily, supported by expectations surrounding the new crop and tighter near-term availability ahead of the main harvest period. This upward movement reflected market anticipation rather than realised supply constraints, with prices reaching elevated levels prior to peak harvest flows.

As harvesting activity progressed, prices began to soften from late February onwards, consistent with increased physical availability entering the market. The downward adjustment accelerated during March and April, as a combination of external disruptions and heightened uncertainty weighed on market sentiment and temporarily slowed trade activity across several key destinations.

Prices reached a short-term low toward the middle of the year, before stabilising and gradually recovering in the second half of 2025. This recovery was supported by easing trade disruptions, adjustments in policy-related measures affecting key markets, and indications of tighter-than-expected supply conditions in selected origins.

Overall, monthly price movements in 2025 underscore the distinction between short-term volatility driven by seasonal flows and external shocks, and the broader structural tightness of the market. While prices fluctuated significantly within the year, the underlying supply-demand balance remained constrained, limiting the extent of sustained downward price corrections.

Prices reached a short-term low toward the middle of the year, before stabilising and gradually recovering in the second half of 2025. This recovery was supported by easing trade disruptions, adjustments in policy-related measures affecting key markets, and indications of tighter-than-expected supply conditions in selected origins.

Overall, monthly price movements in 2025 underscore the distinction between short-term volatility driven by seasonal flows and external shocks, and the broader structural tightness of the market. While prices fluctuated significantly within the year, the underlying supply-demand balance remained constrained, limiting the extent of sustained downward price corrections.

Prices of black pepper reached a cyclical low around mid-2025 before recovering gradually in the second half of the year. While this recovery coincided with easing trade disruptions and adjustments in policy-related measures affecting key markets, it did not signal a fundamental shift in the market's long-term supply-demand balance.

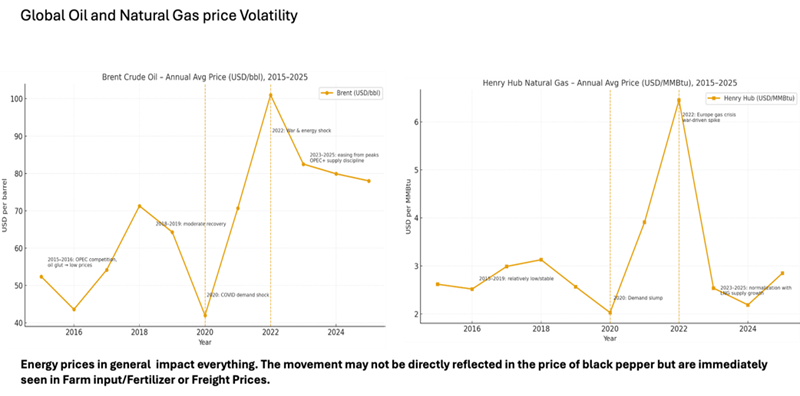

Developments over the period 2020-2025 highlight an important distinction in pepper price formation. While long-term price trends continue to be governed primarily by structural supply and demand fundamentals, short-term price volatility has increasingly been shaped by external shocks, policy adjustments, and macroeconomic conditions.

In this context, energy prices represent a critical transmission channel. As illustrated by trends in global crude oil and natural gas prices, sharp movements in energy markets have had a direct impact on production costs, fertiliser prices, and freight rates. Although these cost pressures may not be immediately reflected in pepper prices, they are rapidly transmitted through farm-level inputs, logistics expenses, and working capital requirements across the supply chain.

The surge in energy prices observed in recent years, followed by partial normalisation, underscores the extent to which cost structures in agricultural commodity markets have become more exposed to global macroeconomic developments. For pepper, this has contributed to a higher underlying cost base, reducing the elasticity of supply responses and amplifying the price impact of even modest disruptions.

Taken together, these dynamics reinforce the importance of viewing pepper price movements through a broader analytical lens. Beyond supply and demand balances, factors such as energy costs, input prices, logistics constraints, and policy environments play an increasingly influential role in shaping short-term volatility, even as long-term fundamentals continue to anchor market trends.

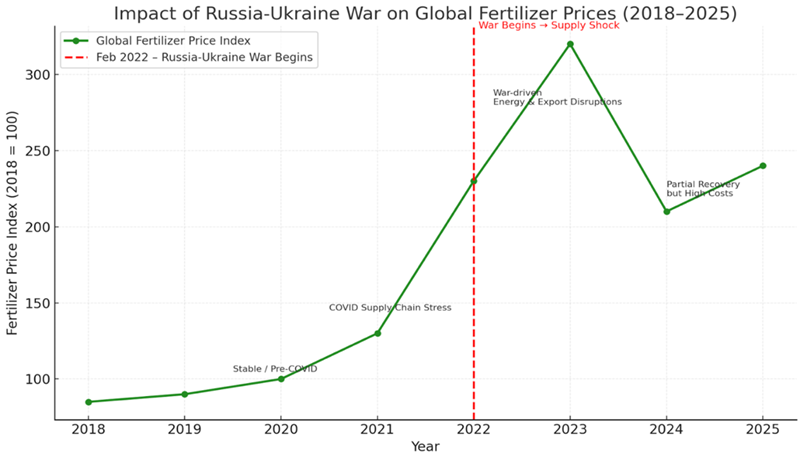

Developments in global fertiliser prices over the period 2018-2025 illustrate a significant shift in the cost structure faced by agricultural producers worldwide, including those in the pepper sector. As shown in the chart, fertiliser prices remained relatively stable in the pre-pandemic period before rising sharply amid supply chain disruptions and broader macroeconomic shocks in the early 2020s.

A pronounced escalation in fertiliser prices emerged from 2022 onwards, driven by a combination of constrained supply availability, higher energy costs, and disruptions to international trade flows. Although prices moderated in subsequent years, they have remained well above pre-2020 levels, indicating a partial normalisation rather than a full return to historical cost conditions.

For pepper producers, elevated fertiliser prices translate directly into higher farm-level input costs. These pressures have affected production decisions, replanting incentives, and yield optimisation strategies, particularly among smallholders with limited access to credit and working capital.

Importantly, the impact of fertiliser price volatility is not always immediately reflected in pepper prices. Instead, cost pressures are often absorbed gradually through reduced input application, delayed farm investments, or lower margins along the supply chain. Over time, however, sustained increases in input costs contribute to a higher structural cost base, reinforcing tighter supply conditions and reducing the elasticity of production responses.

Overall, fertiliser price dynamics have become a critical component of cost transmission within the global pepper value chain. Even as market prices adjust to short-term fluctuations, elevated input costs continue to shape production behaviour and medium-term supply availability across major producing origins.

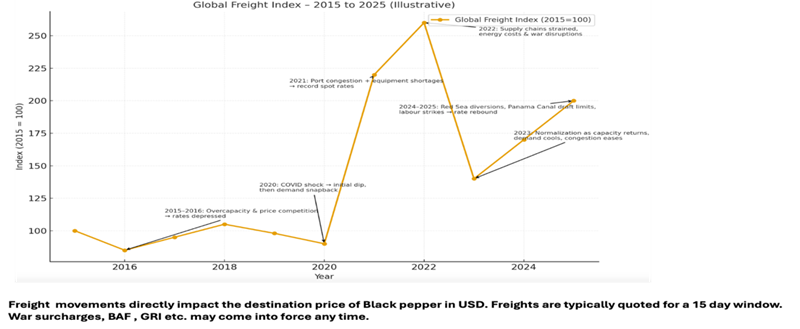

Freight Costs and Logistics Constraints

Freight costs have emerged as a critical transmission channel affecting the price of black pepper delivered in international markets. As illustrated by the Global Freight Index, shipping costs experienced pronounced volatility over the past decade, reflecting shifts in capacity, demand conditions, and external disruptions within global logistics networks.

In the pre-pandemic period, freight rates remained relatively subdued amid ample capacity and competitive pricing. This dynamic changed sharply from 2020 onwards, as supply chain disruptions, port congestion, and equipment shortages led to a rapid escalation in freight costs. The peak observed in the early 2020s underscored the vulnerability of agricultural trade to systemic shocks within global logistics.

Although freight rates moderated as capacity gradually returned and congestion eased, developments during 2024-2025 indicate that logistics costs have not reverted fully to pre-2020 norms. Route diversions, operational constraints at key transit points, and labour-related disruptions have contributed to renewed upward pressure and heightened uncertainty in freight pricing.

For the pepper sector, freight volatility has a direct and immediate impact on destination prices, given the relatively high share of logistics costs in total landed value. The short validity period of freight quotations further amplifies this effect, limiting the ability of exporters and importers to hedge logistics expenses over extended periods.

Beyond headline freight rates, ancillary charges, including bunker adjustment factors, general rate increases, and other surcharges, have become more prevalent, adding complexity to cost planning and contract execution. Collectively, these factors have reinforced a higher and more variable logistics cost base, shaping trade flows and influencing pricing behaviour across the global pepper value chain.

Currency Movements and Exchange Rate Pass-Through

Exchange rate movements have played an increasingly important role in shaping price dynamics and trade behaviour within the global pepper market. As pepper is predominantly traded in US dollars, fluctuations in local currencies directly affect producer revenues, exporter margins, and importer costs across both producing and consuming countries.

Over recent years, heightened volatility in global currency markets, driven by divergent monetary policies, inflationary pressures, and broader macroeconomic uncertainty, has amplified exchange rate risks for market participants. For producing countries, currency depreciation can temporarily enhance export competitiveness by lowering local currency costs, even as input expenses, often denominated in foreign currency, continue to rise.

Conversely, currency appreciation may compress margins for exporters and reduce price competitiveness, particularly in markets where cost increases from fertilisers, energy, and freight cannot be fully passed through to buyers. For importing countries, exchange rate movements influence landed costs and purchasing strategies, contributing to adjustments in sourcing patterns and contract timing.

Importantly, exchange rate effects are not uniform across the value chain. While short-term currency movements may offer tactical advantages or pressures, sustained volatility introduces uncertainty into pricing decisions, contract negotiations, and investment planning. This can lead to more conservative trade behaviour, shorter contract tenures, and increased reliance on spot market transactions.

Taken together, currency dynamics represent a critical layer of cost transmission beyond supply, demand, and logistics factors. In combination with elevated input and freight costs, exchange rate volatility has contributed to a more complex and risk-sensitive trading environment, reinforcing the need for greater transparency, risk management, and coordination across the global pepper value chain.

6. OUTLOOK FOR 2026

Supply:

Vietnam

Despite heightened attention on weather-related developments, including episodes of prolonged rainfall in certain growing areas, no significant decline in overall production is anticipated for 2026. Output is expected to remain broadly comparable to 2025 levels, with any shortfall likely to be limited in scale.

Seasonal export flows may experience some timing adjustments, particularly in the early part of the year, as harvesting activity could be marginally delayed. As in previous years, shipment volumes are expected to increase from late February onwards, with peak flows anticipated during March.

India

Production prospects for India in 2026 remain constrained. Industry assessments point to a continued impact from adverse agronomic conditions, resulting in a notable reduction in output compared to recent years. Domestic absorption is expected to remain strong, limiting exportable availability and reinforcing India's reliance on imports to support downstream processing activities.

Brazil

Brazil is expected to record a favourable crop in 2026, which may partially offset supply constraints in other origins. The southern harvest has already commenced, with exportable volumes projected to increase during the first quarter of the year. Brazil is therefore likely to continue playing a stabilising role in global supply flows, particularly in the early months of 2026.

Indonesia, Malaysia, Cambodia, and Sri Lanka

Production across these origins is expected to remain broadly stable in 2026, with each continuing to serve specific market segments. While overall volumes are relatively modest in comparison to larger producers, these origins remain important for supply diversification and quality differentiation.

At the same time, increased attention to compliance requirements, including pesticide management and residue controls, will remain essential. Changes in intercropping practices and input usage may pose additional compliance challenges, underscoring the importance of continued adherence to good agricultural and post-harvest practices.

Key Takeaways on the Production and Supply Side

- Global pepper production in 2026 is expected to remain broadly in line with 2025 levels, with limited scope for significant expansion.

- Compliance-related risks, including those associated with pesticide residues, are likely to remain an important consideration across multiple origins.

- The availability of compliant, quality-consistent pepper is expected to remain relatively constrained, reinforcing market segmentation.

- Improved farm-gate prices in recent periods have strengthened the financial position of producers, contributing to greater holding capacity and more measured selling behaviour.

- Tighter working capital conditions for exporters and traders are expected to reduce the availability of forward offers, leading to more cautious contracting and greater reliance on spot market transactions.

Demand:

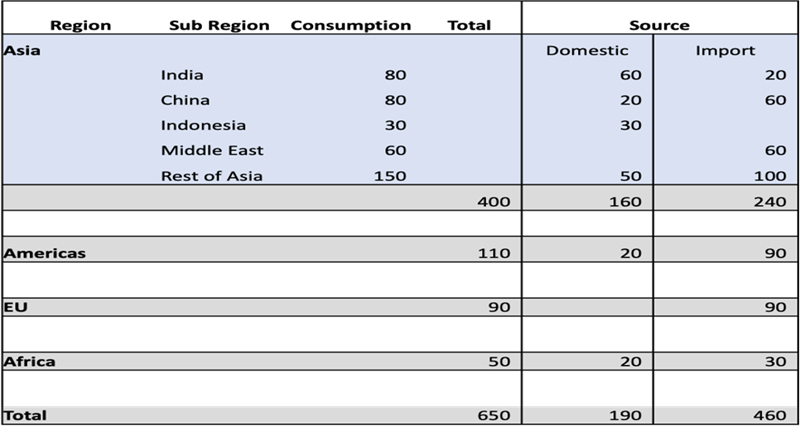

Region wise break up of Global Black Pepper Demand in KMT

Global black pepper demand remains geographically diversified, with Asia continuing to account for the largest share of global consumption. As reflected in the regional breakdown, Asia accounts for approximately 400 KMT, or more than 60 percent of the total global demand, driven by a combination of large domestic markets and well-established processing and distribution hubs.

Within Asia, India and China each account for an estimated 80 KMT of consumption, although their sourcing profiles differ significantly. India relies predominantly on domestic production to meet consumption needs, while China continues to depend largely on imports, reflecting its role as a major consuming and processing market. Other Asian markets, including Southeast Asia and the Middle East, collectively contribute substantial demand volumes, reinforcing Asia's central role in global pepper trade flows.

Demand in the Americas, estimated at around 110 KMT, remains largely import-dependent, underscoring the region's sensitivity to international supply availability and logistics conditions. Similarly, the European Union, with consumption of approximately 90 KMT, relies almost entirely on imports and is increasingly shaped by regulatory and compliance considerations related to food safety and sustainability.

Africa, while accounting for a smaller share of global demand at approximately 50 KMT, continues to exhibit steady growth potential, supported by population expansion and evolving consumption patterns.

Overall, global black pepper demand is estimated at approximately 650 KMT, corresponding to an aggregate market value of around USD 5 billion at average wholesale prices in 2025. Of this total, roughly 70 percent is met through international trade, highlighting the continued importance of cross-border supply chains and market access.

Recent shifts in sourcing patterns, particularly changes in China's import composition, reflect diversification of supply origins rather than a contraction in underlying demand. Increased imports from alternative origins and incremental domestic production have contributed to adjustments in trade flows, while overall consumption levels remain broadly stable.

Global demand for black pepper is expected to continue expanding at a moderate but steady pace, with average annual growth projected in the range of 2-3 percent over the medium term. This growth outlook reflects the essential role of pepper as a staple ingredient in food applications, even amid elevated price levels.

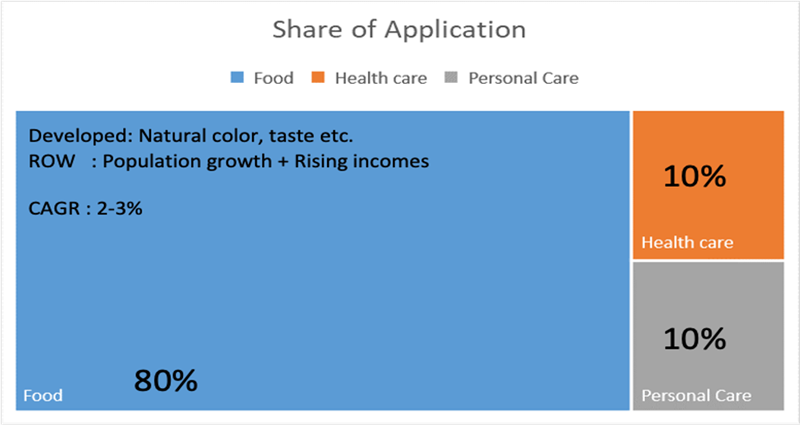

As illustrated in the application breakdown, the food sector continues to account for approximately 80 percent of total black pepper consumption. In developed markets, demand growth is supported by sustained use of natural flavouring, colour, and taste enhancers in food processing and foodservice segments. In emerging and developing economies, consumption is further underpinned by population growth, urbanisation, and rising household incomes.

Beyond food applications, the healthcare and personal care segments together account for roughly 20 percent of total usage. While smaller in absolute terms, these segments are characterised by higher value addition and increasing interest in functional ingredients, contributing to incremental demand diversification.

Freight Outlook 2026

According to projections by the World Bank and the International Monetary Fund, global GDP is expected to expand by approximately 2.8 percent in 2026, providing a broadly supportive macroeconomic backdrop for international trade and logistics.

Key developments shaping the freight outlook include:

- Global container demand is projected to increase by around 5 percent, in line with the anticipated recovery in global merchandise trade.

- The entry of new vessel capacity is expected to expand global fleet availability by approximately 7 percent, easing some of the supply-side constraints observed in recent years.

- Progressive normalization of key maritime routes, including the gradual reopening of Red Sea corridors, is anticipated as regional conditions improve.

- Despite the increase in capacity, freight rates are not expected to decline sharply, as port congestion, route adjustments, and ancillary surcharges may continue to exert upward pressure on costs.

- Freight market volatility is likely to persist, reflecting ongoing adjustments in trade policies and shifts in global trade routes, particularly as Asian exporters diversify destination markets. Freight rates from Asia to the United States are expected to remain within a relatively lower range compared to recent peaks.

Overall, while localized disruptions and short-term volatility cannot be ruled out, freight conditions in 2026 are expected to be broadly manageable and are not anticipated to constitute a major structural constraint on global black pepper trade.

Currency Outlook 2026

The US dollar is expected to face moderate pressures in 2026, reflecting a combination of evolving macroeconomic conditions and monetary policy dynamics. As global growth momentum broadens and monetary policy in the United States gradually normalises, currency markets are increasingly pricing in a reduced divergence between the US and other major economies.

Recent indicators show that the dollar's real broad effective exchange rate, which measures its value against a basket of major currencies, adjusted for inflation-has eased from its recent peak. While the dollar remains relatively strong by historical standards, this moderation suggests a gradual adjustment rather than a sharp reversal, consistent with a more balanced global growth outlook.

Expectations of a softer dollar environment are closely linked to converging growth trajectories across major economies. Policy support measures in Europe, continued macroeconomic adjustments in China, and improving growth prospects across parts of the euro area are expected to narrow the relative growth advantage previously enjoyed by the United States. This dynamic has historically reduced upward pressure on the US dollar.

Despite intermittent rebounds observed in recent months, foreign exchange strategists broadly anticipate a more neutral to mildly weaker dollar trend in 2026, influenced by monetary policy recalibration by the Federal Reserve, narrowing growth differentials, and valuation considerations.

From a commodity trade perspective, a less elevated dollar environment would provide modest relief for importing markets, potentially supporting demand stability while reducing currency-related cost pressures along global supply chains.

Currency Developments Across Key Black Pepper Origins

Brazilian Real (BRL)

The Brazilian real strengthened notably against the US dollar during 2025, appreciating from approximately 6.2 to 5.2 by November, before easing modestly to around 5.54 in December. On an annual basis, this represents an appreciation of close to 11%, reflecting improved market sentiment and capital inflows into Brazil.

Looking ahead to early 2026, the Brazilian real is expected to trade within a relatively narrow range, broadly between 5.0 and 5.5 against the US dollar. Currency movements within this range will remain an important factor in determining the relative competitiveness of Brazilian pepper exports, as further depreciation could provide additional flexibility in USD-denominated pricing, while currency strength may moderate exporter margins.

Vietnamese Dong (VND)

The Vietnamese dong has remained comparatively stable, albeit with a gradual appreciation bias. Analysts at United Overseas Bank (UOB) continue to maintain a cautious outlook, projecting USD/VND levels of approximately 26,300 in Q1 2026, strengthening gradually to around 25,900 by Q4.

A firmer Vietnamese dong would have cost implications for international buyers, as currency appreciation may translate into higher USD-denominated export prices, even in the absence of changes in underlying domestic market fundamentals. As a result, currency dynamics are expected to remain a relevant consideration for trade flows and pricing discussions involving Vietnam-origin pepper in 2026.

Indonesian Rupiah (IDR)

Indonesia's macroeconomic fundamentals remain relatively resilient, supported by steady GDP growth, adequate foreign exchange reserves, and continued expansion in export performance. These factors have contributed to a broadly stable outlook for the Indonesian rupiah entering 2026.

Monetary authorities, including Bank Indonesia, have signaled confidence in maintaining currency stability through a combination of prudent monetary policy, calibrated market interventions, and close monitoring of external developments. While short-term fluctuations remain possible, the rupiah is expected to trade within a manageable range, reflecting both domestic fundamentals and global financial conditions.

From a trade perspective, a relatively stable to mildly firmer rupiah would support macroeconomic confidence while potentially moderating exporter margins in USD terms. As such, currency developments are expected to remain a relevant, though not dominant, factor shaping Indonesia's competitiveness in global pepper markets in 2026.

Key Currency Takeaway

Looking ahead to 2026, a broad-based depreciation of origin currencies is not widely anticipated. Instead, several producing countries may experience stable to mildly firmer currency conditions, particularly in a scenario where global monetary policy becomes more accommodative and interest rate differentials narrow, including potential further easing by the Federal Reserve.

In this context, currency movements are expected to influence pricing dynamics at the margin, rather than drive structural shifts in trade flows. Market participants are therefore likely to place greater emphasis on supply fundamentals, logistics conditions, and regulatory compliance as key determinants of competitiveness in 2026.

Price Outlook: Black Pepper 2026

Bullish Elements

- Production in key origins is expected to remain broadly similar or slightly lower compared to 2025, with limited carry-over stocks, particularly in Vietnam.

- Demand conditions are normalizing amid fewer geopolitical disruptions and the absence of major tariff-related constraints, supporting modest consumption growth.

- A relatively weaker US dollar environment may lend marginal support to commodity prices in USD terms.

- Structural supply constraints persist, with no significant expansion in plantation area observed across major producing regions.

- Farmers across origins have benefited from stronger returns across multiple crops, enhancing holding capacity and reducing immediate selling pressure.

- Market visibility remains concentrated primarily within the first half of 2026, limiting forward coverage beyond Q1.

Bearish Elements

- Elevated price levels may continue to exert pressure on working capital for traders and exporters, moderating near-term buying appetite.

- Seasonal supply inflows are expected in early 2026, with Brazil's crop entering the market in January-February and Vietnam's peak harvest occurring in March-April, potentially increasing availability during Q1-Q2.

- Higher absolute price levels may reduce speculative participation as returns on short-term trading positions become less attractive.

Overall, Price Assessment

Taking these factors together, price movements in 2026 are expected to remain firm but measured, with limited downside risk and selective upside potential. Seasonal softness may emerge during peak harvest periods in the first half of the year; however, structural supply tightness, low carry-forward stocks, and improving demand conditions are likely to provide underlying support as the year progresses.

Price strength is therefore expected to be more consolidation-driven than speculative, with market direction increasingly shaped by physical availability, inventory positions, and shipment timing rather than abrupt sentiment shifts.

Brazil Supply Dynamics

Brazilian origin remains largely committed for early 2026, with January shipments effectively covered and limited availability extending into February-March. With a significant portion of the crop already marketed, some shipment pressure may persist in the first quarter. Fresh Brazilian supply is expected to re-enter the market more meaningfully only in the latter part of the year, reinforcing a relatively balanced supply outlook through mid-2026.

Pepper Trade Statistics of Major Producing Countries

PEPPER TRADE STATISTICS OF MAJOR PRODUCING COUNTRIES

Trade Flow Patterns and Market Concentration

Trade statistics for 2025 reaffirm the central role of a limited number of markets in shaping global pepper trade flows, while also highlighting distinct structural differences among major producing countries.

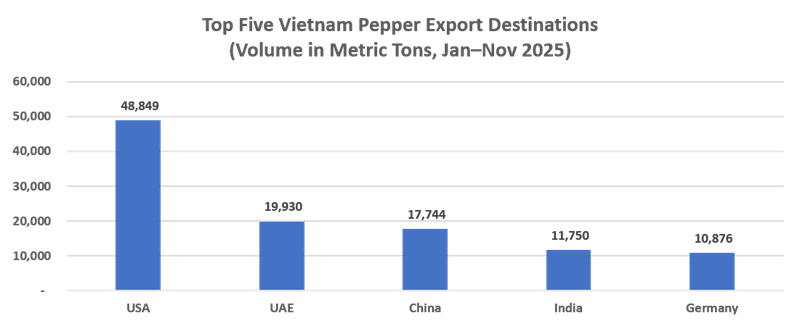

Vietnam continues to demonstrate a highly diversified export profile, with the United States remaining its largest single destination. Strong and consistent volumes to the USA, alongside significant flows to the UAE, China, India, and Germany, underscore Vietnam's position as the most globally integrated supplier. The prominence of both mature markets (USA, Germany) and trading hubs (UAE) reflects Vietnam's ability to serve a broad spectrum of demand, from direct consumption to re-export and distribution channels.

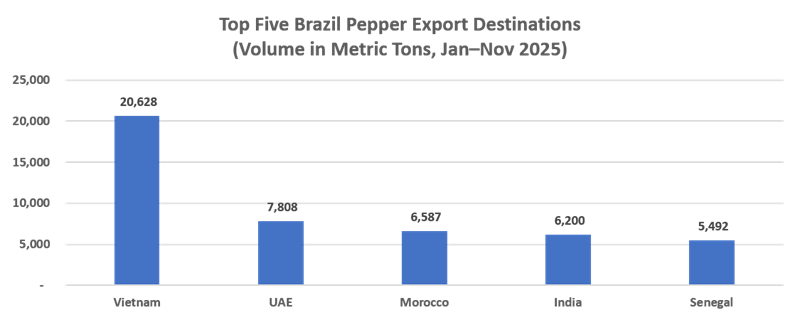

Brazil's export structure, by contrast, appears more concentrated and regionally differentiated. Vietnam emerges as Brazil's largest destination, highlighting strong inter-origin trade linkages and Brazil's role as a complementary supplier during periods of tight Asian availability. Exports to the UAE, Morocco, India, and Senegal further illustrate Brazil's growing importance in supplying price-sensitive and emerging markets, particularly in Africa and the Middle East.

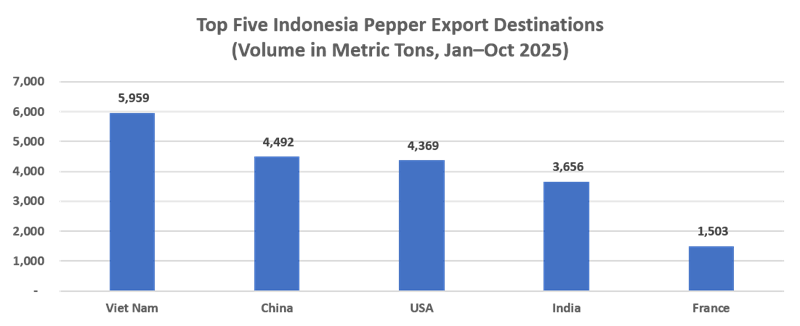

Indonesia's export pattern reflects a more niche-oriented and selective market positioning. Volumes remain modest relative to Vietnam and Brazil, with shipments primarily directed toward Vietnam, China, the United States, India, and France. This distribution suggests Indonesia's continued focus on specific quality segments and established bilateral trade relationships rather than large-scale volume expansion.

Key Trade Insights

Overall, the data point to a high degree of demand concentration in a small number of consuming and trading hubs, notably the United States, China, Vietnam, and the Middle East. The continued importance of intermediary markets, particularly the UAE, highlights the role of re-export and redistribution in the global pepper value chain.

At the same time, inter-origin trade flows, especially between Brazil and Vietnam, signal a maturing and increasingly interconnected global pepper market, where origins are not only competitors but also strategic counterparts in balancing supply across seasons.

Global Pepper Market: From Volatility to Structural Balance

The 2025 review and 2026 outlook highlight a global pepper market transitioning from episodic volatility toward a more structurally balanced phase. While short-term disruptions, ranging from geopolitical tensions to trade policy shifts, have continued to influence price movements and trade flows, the underlying fundamentals of supply and demand remain broadly intact.

On the supply side, production across major origins is expected to remain broadly stable in 2026, with no material expansion in planted area and limited carry-forward stocks in several key producing countries. Structural constraints, rising compliance requirements, and increasing production costs suggest that supply responsiveness will remain limited in the near term, reinforcing a firmer underlying market tone.

From a demand perspective, consumption growth is projected to continue at a moderate but steady pace, supported by population growth, income expansion in emerging markets, and the resilience of food-sector demand globally. While speculative activity may fluctuate in response to price levels and macroeconomic conditions, physical demand remains anchored in essential consumption patterns rather than discretionary use.

Price dynamics entering 2026 are therefore expected to be shaped less by abrupt shocks and more by seasonal supply flows, inventory positioning, and currency movements. Although periods of short-term softness may emerge during peak harvest windows, the absence of surplus production and the persistence of structural supply tightness are likely to limit sustained downside risks.

At the same time, trade flows continue to reflect a high degree of concentration in key consuming and distribution hubs, notably the United States, China, Vietnam, and the Middle East. The growing importance of inter-origin trade and re-export channels underscores an increasingly interconnected global pepper market, where coordination across origins plays a critical role in balancing availability across seasons.

Looking ahead, macroeconomic conditions, including expectations of global growth recovery, easing monetary policy in major economies, and relative currency stability, provide a supportive backdrop for the pepper sector in 2026. Freight and logistics constraints, while still relevant, are no longer expected to be a dominant market disruptor, shifting attention back to core supply-demand fundamentals.

Concluding

Overall, the global pepper market enters 2026 with measured optimism. The year ahead is likely to be characterized by consolidation rather than exuberance, with prices, trade flows, and production responding to structural signals rather than speculative excess. For producers, traders, and policymakers alike, this environment underscores the importance of strategic positioning, disciplined risk management, and continued attention to sustainability and compliance as defining factors for long-term market resilience.

Sources and Notes

- Market intelligence and trade insights are derived from a combination of industry inputs, including contributions from Namagro Trading Ltd., alongside data compiled and maintained within the IPC database.

- The International Pepper Community (IPC) does not set or recommend pepper prices. IPC publishes prevailing market prices and statistical information as reported by official national sources, industry stakeholders, and other reliable references.

- All figures presented reflect prevailing market conditions at the time of reporting and are subject to revision as additional information becomes available.

- Data has been processed, validated, and cross-referenced in accordance with IPC's internal statistical and reporting standards.

This publication is intended to provide market information and analytical perspectives. The International Pepper Community does not issue investment advice, price recommendations, or official market forecasts. Any interpretation or use of the information contained herein remains the responsibility of the reader.

Previous Publications

- GLOBAL PEPPER MARKET REPORT ANNUAL REVIEW 2025 AND OUTLOOK 2026

- Global Pepper Report - First Half January to June FY 2025

- GLOBAL PEPPER INDUSTRY SEMESTERLY REPORT

- GLOBAL PEPPER INDUSTRY 3RD QUARTERLY REPORT (JULY - OCTOBER 2022)

- WORLD PEPPER INDUSTRY 2ND QUARTERLY REPORT (JAN -JUNE 2022)

- 1st Quarterly 2022 Report

- 3rd Quarterly 2021 Report

- 2nd Quarterly 2021 Report

- 1st Quarterly 2021 Report

- 4th Quarterly 2020 Report

- 3rd Quarterly 2020 Report

- 2nd Quarterly 2020 Report

- 1st Quarterly 2020 Report

- 4th Quarterly 2019 Report

- 3rd Quarterly 2019 Report

- 2<sup>nd</sup> Quarterly 2019 Report

- 1<sup>st</sup> Quarterly 2019 Report